Stop building what VCs want

Stop building what VCs want

Why we're busy breeding mice instead of building for customers

Hey, Toni from Growblocks here! Welcome to another Revenue Letter!

This weekly email is my way to share knowledge and build a community of people who love to learn more about growing revenue in a data-driven and scientific way.

Anything in particular you want to hear my thoughts on? Drop me an email, and I might use it in my next article.

Have you heard about Goodhart’s law?

It works like this:

Say you want to get rid of mice in a city.

So you decide to pay a bounty for handing in dead mice.

But what ends up happening? People start breeding mice.

When a measure becomes a target, it ceases to be a good measure.

That’s also what happened to VC-backed companies.

VCs valued what great companies looked like:

Great Net Retention

Rule of 40

Rapid YoY Growth

So we started doing things that deliver those metrics, but for the reasons VCs intended:

NRR: Unjustified price increases and NRR hacking (ultra-low initial deal) vs. growing through a great product and customer experience

Rule of 40: Overspending on Sales & Marketing by cutting Product vs. investing in building a great product

ARR: Scaling everything that returns some money vs. scaling channels that are ROI positive

None of the above is the right thing for the customer. And while we know this won't work in the long run, it will work for now.

Because, hey, we can easily get more cash, right?

Well, that reality changed. And VCs flipped their “investment thesis” upside down in the time it takes to write a Tweet.

Why did they do that? Because their customers changed their tune as well. And their customers are the Public markets. Either public players buying your investment or the full-fledged IPO.

These public markets suddenly said, well, you know, actually, growth isn’t all that important. What is important is that you build a solid company with “profits.”

And how do you do that?

Efficiency of your Channels

Sustainability of Scale

Strong Product Market fit

In other words, a full 180° on expectations.

This kicked off three separate waves.

Wave 1: 2022 the Shock: "default alive" was the motto

In the beginning, it all just felt like a blip, “surely, in 12 months, we will be back to normal”.

The problem with this approach is that many bigger changes kind of don’t make sense. 12 months of ramp-down and then ramp-up again is silly. So what did we do?

We scaled everything down a bit but kept the same structures in place. Essentially playing the same playbook but with less cash burn.

Which meant that real change - basically stalled for a year.

Then in 2023:

Wave 2: 2023 the Adjustment: Growth at all Costs (GaaC) is over

I think we all woke up in 2023 realizing at some point that the “old normal” might simply not return.

The “GaaC-Movement” started. We all suddenly realized how silly we were just 2 years ago.

This triggered the 2nd wave of change. This time it was a structural change: We rebuilt our GTM.

We suddenly decided outbound didn’t work, or ads on Meta didn’t work, or whatever. We scaled the parts down that didn’t return enough money.

All this change was pretty good. Lots of aha moments in the industry.

I think this wave sometimes gets a bit mixed up with “AI” - but really this is just a phenomenon that happened while this was going on. It wasn’t causing or changing anything.

We only recently started seeing AI having a real impact on company performance (e.g. ServiceNow).

And then finally:

Wave 3: 2024 the Calibration: Finding GTM Fit (again)

The Calibration wave simply has to follow the Adjustment Wave. No chance we will be getting everything right in one go.

Lots of new motions, and tons of GTM changes were executed.

Some worked out and some didn’t. Totally normal.

What we are all doing is trying to figure out GTM-Fit (again). Some if not all of us will get it wrong somewhat.

But if I am right, this should be the last real “wave”. Or rather the last ripple of the 2022 correction in SaaS.

What will happen next is pretty clear, we are back to “normal” pre-2019 days and companies have adjusted their set-up to match that.

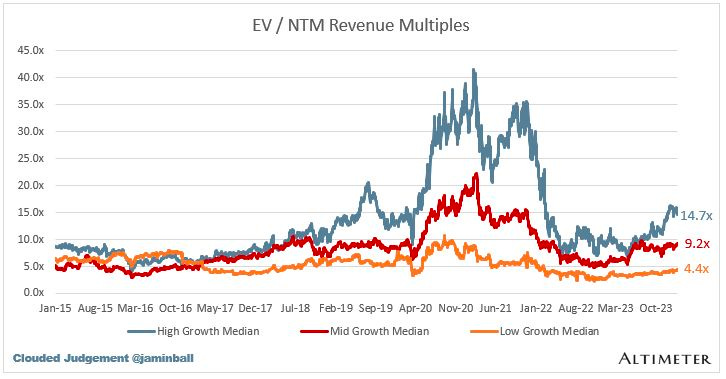

And latest data is even showing some signs that we will settle at or a a bit above the pre-COVID times:

The larger problem with that though: a lot of VCs actually also don’t know how this will play out for them.

I recently talked to a VC who said “Toni, I am not sure I’ll have a job in 5 years - sure Sequoia, Index, and Bessemer will be around, but does the industry need all of us?”

And the root cause is simple: it’s not only a bunch harder to build a company with less cash. But it is even harder to find companies that can build up to 100M ARR in 6-7 years to return a VC fund during its lifespan. Because this is exactly how their economics work.

Ultimately, this all means that

Let’s go back to building good & solid businesses

Let’s do that by focusing on what our customers want

Let’s scale as fast as we can, but without being silly

And I think to do that you will need 2 kinds of very deep experts in every business.

You will need a product leader who doesn’t only understand how to build stuff but also how to deliver value to the users & customer

And you will need a deep expert in GTM.

A GTM expert is a profile that:

understands which motion

in which situation makes sense to execute

towards what persona and ICP

under what unit economic limitations

And then is able to execute that across

people

process

tools

and data

This really is the reason why I can’t see a “pure” VP Sales being this person.

I think this requires a CRO-type. And yes I also think this could be done by a RevOps profile that can be strategic.

What I am hoping to achieve with this newsletter is that we will have more fully rounded profiles that can go out and build these companies.

P.S. We’ve been building Growblocks with this new reality in mind. Find every problem in your GTM engine with one click, and easily build your plan and set expectations for every metric across your funnel. Book a demo or email me to learn more.

This is a great article! Well done Toni, so well articulated! Your definition of a “GTM Expert” is excellent and a high standard for people to achieve, as it should be.